What We’ve Learned About Superannuation Goals & choices

Here, we share experiences and insights, learning from each other’s journeys rather than offering advice.

Superannuation often sits quietly in the background but deserves far more attention. The decisions you make today, from how your super is invested to the fund you select, quietly shape your financial future. It’s not just about retirement. It’s about securing choices and opportunities for the years ahead. Give your future self the gift of good choices today.

A better pension tomorrow starts with smart super choices today. ➔➔➔

Session Breakdown

Return and Risk Objectives

Required return (%) = Inflation Rate + Target Real Return

+ Fund Expenses + Insurance Costs (if applicable)

+ Drawdown Rate (for retirees)

Required/Target return ≠ Expected return

Required return aligns with your desired living standard.

Expected returns are subjective and may be unreliable.

Switch funds if performance falls short

You have the option to select different in-house investment

strategies or even switch your superannuation fund.

Investment horizon – long-term by nature.

The primary objective of a superannuation fund is to achieve long-term returns that grow members’ retirement savings while prudently managing risk in line with regulatory obligations and members’ financial goals.

Required returns matter, expected returns are uncertain.

Long-term capital preservation and real growth are essential for securing your financial future. Inflation, fees and taxes can gradually erode the value of your superannuation balance over time, making it crucial to ensure that your chosen asset allocation can at least preserve and ideally grow your super balance in real terms.

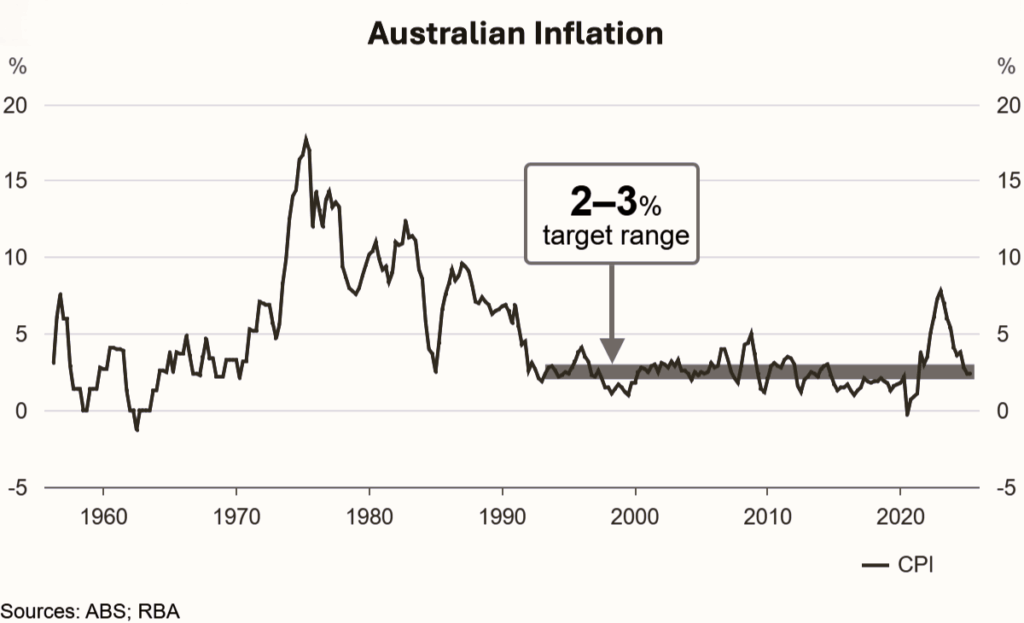

Returns need to exceed inflation to preserve purchasing power amid rising prices of goods and services. This should be considered a minimum requirement/target. It is also important to review the management expenses charged (0.4% – 1.5% p.a.) by your super fund, as these can impact your overall returns.

Since the expected returns provided may not always materialise, ongoing monitoring of your superannuation performance is essential.

The ability to take risk sets objectives.

To avoid experiencing unexpected downside risk, your ability to take risk should be carefully assessed. Seeking advice from a qualified financial advisor may be helpful. Do not let your willingness to take risks outweigh your capacity to manage them.

Asset Allocations

Asset allocations need to match return goals and risk

appetite to achieve long-term target outcomes.

Age and stage of the life cycle often affect which

investment bucket is most appropriate. Risk tolerance

and financial goals typically change over time.

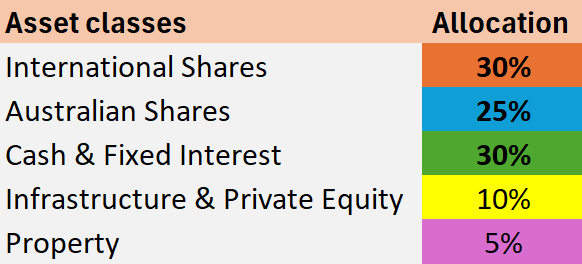

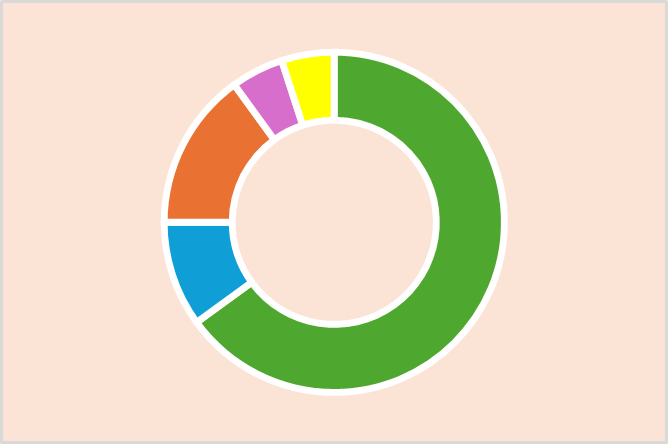

Conservative/Defensive Bucket

The conservative or defensive bucket in superannuation focuses on preserving capital and minimizing risk by investing mainly in low-risk asset classes such as cash equivalent and fixed interest. This approach offers stable returns and protects the fund during market downturns, making it suitable for those with lower risk tolerance or approaching retirement. However, its lower risk profile also means slower growth potential compared to growth-focused investments, which may limit long-term wealth accumulation.

Balanced Bucket

The balanced bucket combines growth and defensive asset classes to deliver moderate risk and returns. It aims for steady growth while managing volatility, making it suitable for those seeking a balance between growth potential and capital protection. Diversification across both growth and defensive asset groups reduces risk while maintaining growth opportunities. This strategy supports consistent portfolio performance through varying market conditions.

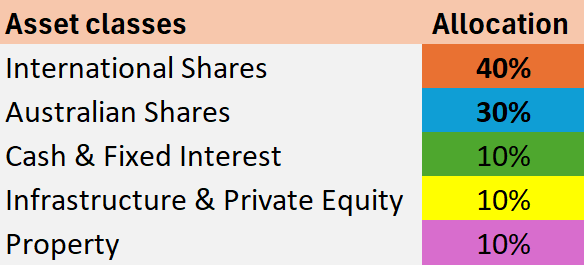

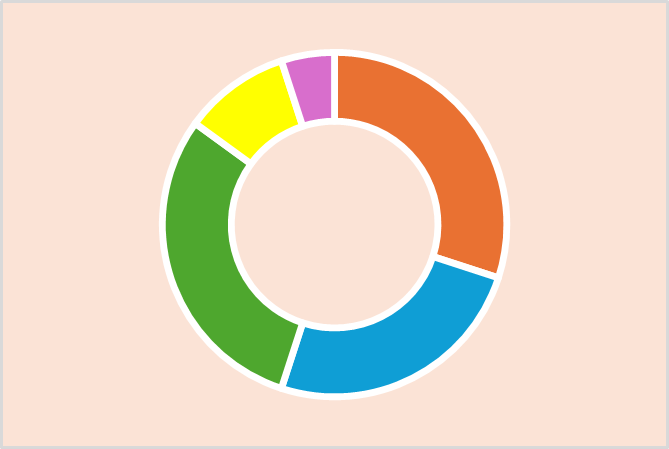

Growth/Aggressive Bucket

The Growth or Aggressive bucket focuses on maximizing long-term returns by investing primarily in higher-risk, growth-oriented asset classes such as shares and property. This approach aims for significant capital appreciation but comes with higher volatility and risk of short-term losses. It is suitable for those with a higher risk tolerance and a longer investment horizon, seeking to build wealth over time despite market fluctuations.

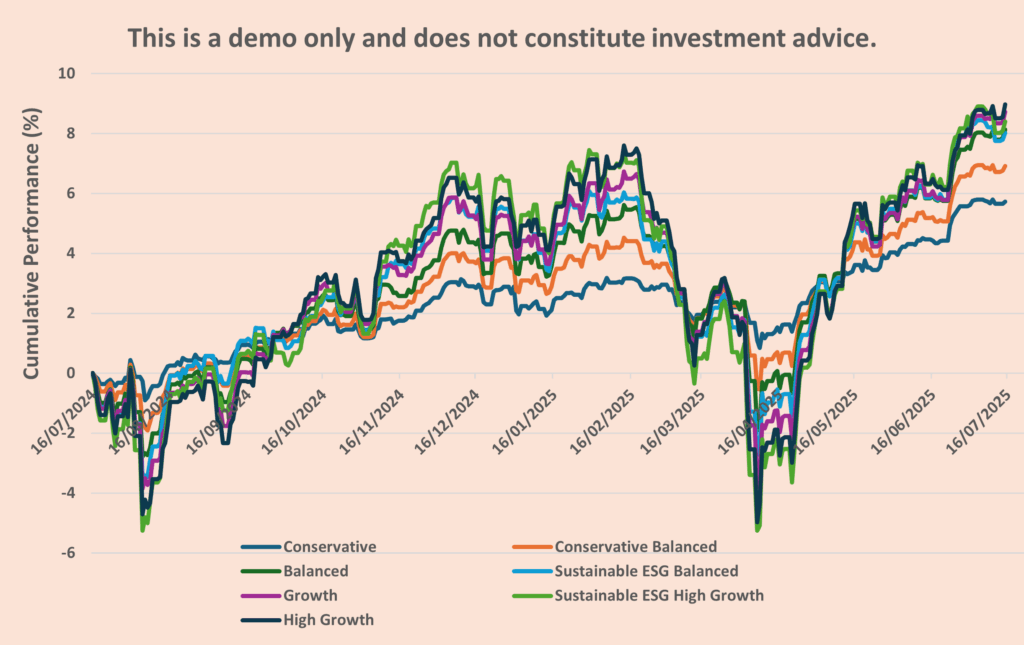

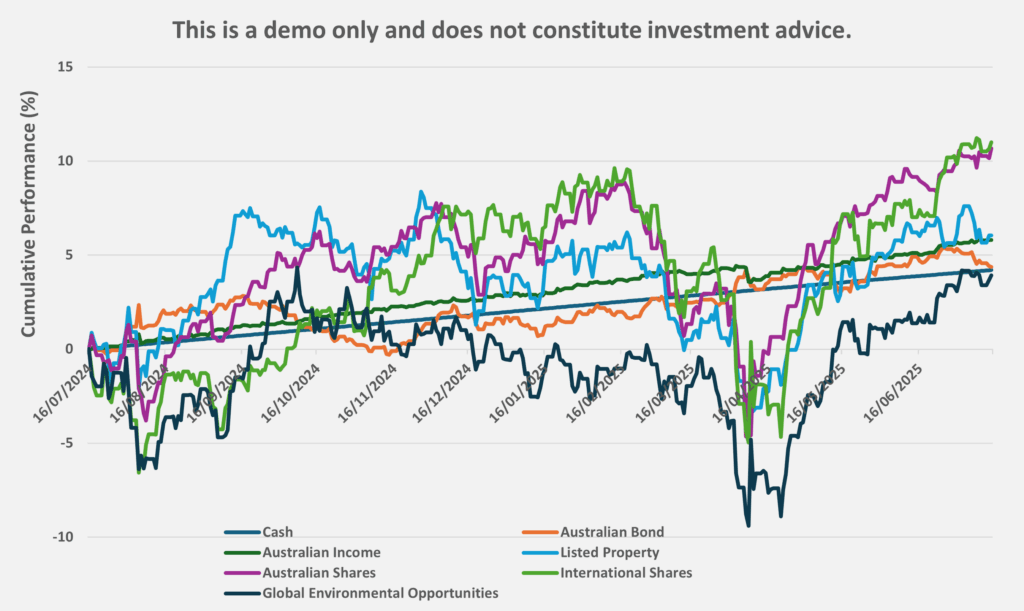

For Demonstration Purposes Only

Asset Allocation Breakdown

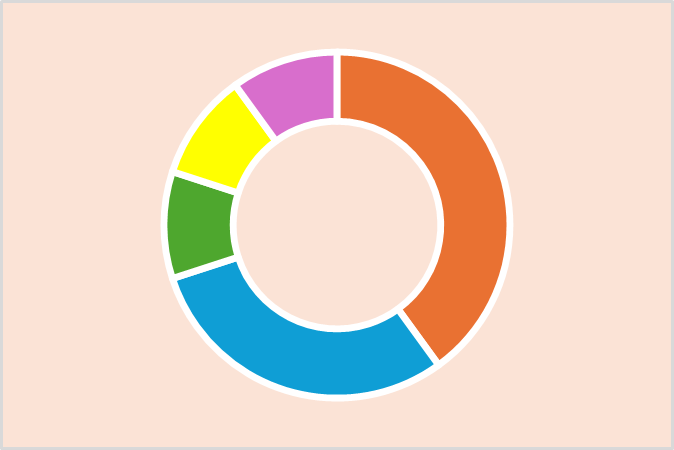

Conservative Bucket

Mainly allocated to defensive assets, prioritising stability over growth.

Real capital growth is constrained by inflation, taxes and investment expenses.

Balanced Bucket

A balanced allocation across growth and defensive assets.

Real capital growth is possible over the medium to long term, despite short-term volatility.

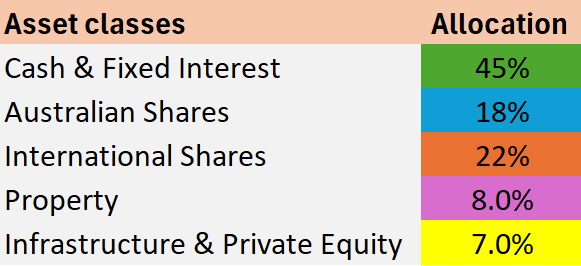

Growth Bucket

Mainly allocated to growth assets, prioritising higher returns.

Real capital growth is possible in the short term, but involves heightened volatility.

Conservative Target

Objective: Outperform CPI by 1% – 1.5% p.a. over 5 years.

Minimum investment timeframe:

At least 5 years

Balanced Target

Objective: Outperform CPI by 3% – 3.5% p.a. over 10 years.

Minimum investment timeframe:

At least 10 years

Growth Target

Objective: Outperform CPI by 4% or more p.a. over 7 years.

Minimum investment timeframe:

At least 7 years

It is important to check the return target and the recommended minimum investment horizon provided by your superannuation fund. The target may not be achieved in the short term, which is why the minimum investment horizon should be treated as a key constraint.

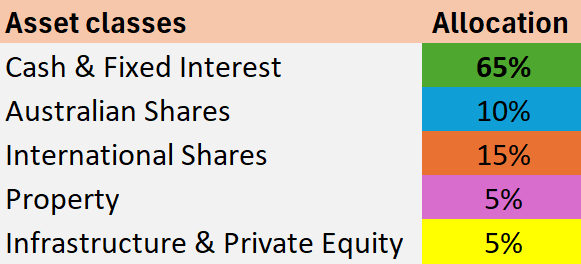

For Demonstration Purposes Only

Other Possible Variants

Conservative Balanced

This option lies between the conservative and balanced buckets.

More growth-oriented than conservative alone & less volatile than balanced alone.

A HYBRID strategy that balances stability with moderate growth potential.

High Growth

This strategy is less diversified and heavily concentrated in the equity market to pursue real capital growth.

A high level of risk tolerance is required.

Stay cautious – DOWNSIDE risk can be significant during equity market downturns.

Sustainable ESG

Focus on achieving long-term financial returns while also considering environmental, social and governance (ESG) factors.

Typically AVOID industries such as fossil fuels, tobacco, gambling and weapons, to promote sustainability.

Asset Classes

Core & Alternative

Superannuation funds typically offer members a choice of

investment options, each with its own asset allocation

(e.g. Conservative, Balanced, Growth).

The fund itself controls the available asset classes, such

as shares (both Australian & International), property,

cash & fixed interest, and infrastructure & private equity.

Members generally can’t directly pick or remove asset

classes themselves unless they’re in a self-managed

super fund (SMSF).

Alternative assets diversify investment portfolios by providing

exposure to asset classes outside traditional stocks, bonds, and cash.

They often offer potential for higher returns, lower correlation with

conventional markets and unique risk-return profiles, contributing to

reduced overall portfolio volatility and enhanced long-term growth.

Cash & Fixed Interest (core defensive)

Cash includes funds held in bank deposits and short-term money market instruments, which may generate interest. Bonds are loans to a company or government that pay regular interest, known as coupon payments. They have a set ‘face value’ at issue, which is repaid at maturity if the issuer doesn’t default. If sold before maturity, you receive the market value, which may be higher (capital gain) or lower (capital loss) than the face value.

Listed Shares (core growth)

Listed shares represent equity ownership in companies traded on public stock exchanges. Returns are typically generated through capital growth from rising share prices and income from dividends. Share prices can fluctuate due to factors such as company performance, market trends, and economic conditions.

Holding a mix of Australian and international shares can provide diversification benefits by spreading exposure across different markets and economies.

Property (alternative)

Property investments include land, real estate, or real property across sectors such as industrial, retail, office, residential, healthcare, logistics, hospitality, data centers and alternative sectors. These holdings can be direct or indirect, often through real estate investment trusts (REITs). Returns generally arise from rental income and capital growth.

Private Equity (alternative)

Private equity involves investing in companies that are not publicly listed. Investments are typically made through partnerships with specialized private equity managers using three main approaches:

- Allocating capital to funds managed by top-tier private equity firms.

- Co-investing alongside these managers.

- Co-underwriting deals to increase exposure and actively manage assets.

Together, these strategies aim to deliver long-term returns that can outperform listed equities.

Infrastructure (alternative)

Physical infrastructure assets include essential services such as roads, tollways, and airports. These investments typically generate returns through user fees, tolls or service charges, combined with potential long-term capital appreciation.

Strategies & Tactics

Extra layer of diversification

Diversification reduces return volatility by offsetting losses in some investments with gains in others.

Strengthen your superannuation by spreading allocations across a wider range of asset classes and markets. Global diversification, which involves investing in assets across different countries and regions, can reduce risk and stabilise long-term returns by tapping into varied economic cycles and growth opportunities.

Timing the market – Staying Calm When Markets Aren’t.

Growth asset classes tend to outperform during market upturns, while defensive asset classes typically perform better during downturns.

Shifting between growth and conservative buckets based on economic cycles is a strategy used to attempt market timing.

Insurance

Superannuation often includes insurance cover such as life insurance, total and permanent disability (TPD) cover, and income protection. These policies provide financial support in the event of death, serious illness, or loss of income due to injury.

Insurance through super – Moneysmart.gov.au

Life cover – Moneysmart.gov.au

Total and permanent disability (TPD) insurance – Moneysmart.gov.au

Income protection insurance – Moneysmart.gov.au

It is important to review your coverage regularly to ensure it meets your individual needs. If your default cover is insufficient, consider purchasing additional insurance for better protection.

Self-Managed Super Fund (SMSF)

At least $200,000 is needed for an SMSF to be cost-effective.

A Self-Managed Super Fund (SMSF) is a private superannuation fund that you manage yourself, offering greater control over how your retirement savings are invested. SMSFs give members the ability to choose and manage their own investments.

An SMSF can have a maximum of six members. All members must act as either individual trustees or as directors of a corporate trustee of the fund. This provides greater flexibility for larger families and more complex estate planning.

However, the flexibility comes with responsibility, as SMSF trustees are legally obligated to comply with superannuation and tax laws, manage administration, complete reporting duties, and implement an appropriate investment strategy in line with regulatory requirements.

Compare SMSFs with other super funds | Australian Taxation Office

Self-managed super funds | Australian Taxation Office

Self-managed super fund (SMSF) – Moneysmart.gov.au

*SMSF record-keeping requirements: Financial records to keep for a minimum of 5 years & Trustee records to keep for a minimum of 10 years.

SMSF record-keeping requirements | Australian Taxation Office

Free Resources

In-house tools and educational resources

Every superannuation fund gives its members the opportunity to access resources, tools, and educational content to better understand and manage their retirement savings. Be sure to check your fund’s official website for the latest resources and updates.

ASIC’s Moneysmart

Moneysmart is a free, independent financial education website created by the Australian Securities and Investments Commission (ASIC).

How super works – Moneysmart.gov.au

Choosing a super fund – Moneysmart.gov.au

Getting your super – Moneysmart.gov.au

Financial Information Service (FIS)

The Financial Information Service (FIS) is a free, confidential, and independent service provided by Services Australia. It helps individuals better understand superannuation and plan for retirement.

Compare and Switch Super Fund

ATO’s YourSuper Comparison

MySuper product is a government-approved, low-cost, and simple

superannuation option introduced under the Stronger Super reforms

in 2012. Most super funds provide MySuper product, and it serves

as the default investment choice unless you select an alternative.

MySuper accounts typically offer either a ‘single diversified’

investment strategy or a ‘lifecycle’ investment approach.

ATO’s YourSuper Comparison (free, government-run)

The ATO’s YourSuper Comparison Tool assists you easily compare fees, performance, and features of superannuation funds to make informed choices.

Canstar (a for-profit comparison service)

Canstar is an Australian financial comparison and ratings company that provides consumers with free tools and star ratings to compare a wide range of financial products, including superannuation funds.

This is a for-profit comparison service. Product providers may pay to appear or advertise, but ratings and comparisons are based on Canstar’s independent research methodology.

How to switch between super funds

Contact the new superannuation fund you want to join, as they usually manage the transfer or consolidation (rollover) process on your behalf, including contacting your old fund to arrange the switch. You will need to complete a rollover or transfer form available on their websites.

Your new super fund usually simplifies the process by managing most steps for you when you ask them to handle the rollover or consolidation.

If the situation is more complex, such as involving lost or unclaimed super, multiple accounts, or tax issues, it is important to consult the ATO’s detailed instructions to ensure the transfer or consolidation is handled correctly and complies with all legal requirements.

Transferring or consolidating your super | Australian Taxation Office

Major types of superannuation funds

Industry funds: Operated on a not-for-profit basis, they redistribute earnings back to members, typically resulting in lower fees and competitive long-term performance. They offer straightforward default investment options and are accessible to all members. However, they may provide limited investment flexibility and less tailored financial advice, which may not be ideal for individuals with complex financial needs or larger superannuation balances.

Retail funds: Typically operated by for-profit financial institutions, retail funds aim to generate returns for shareholders while offering a wide range of investment options. They often provide personalised financial advice and services but generally charge higher fees compared to industry funds. Retail funds may suit members seeking diverse investment choices and tailored advice, although fees can impact net returns, especially for smaller account balances.

Corporate funds: Established by employers, corporate funds are designed to provide superannuation benefits specifically for their employees. These funds may be managed internally or outsourced to professional super fund managers. Corporate funds often offer tailored investment options and benefits aligned with the employer’s workforce needs. While fees and features vary, they typically provide a balance between personalised service and cost efficiency, making them suitable for employees of larger organisations.

Public sector funds: These superannuation funds cater primarily to government employees and often include defined benefit schemes alongside accumulation accounts. They typically offer low fees, stable returns, and comprehensive member benefits reflecting their public sector focus. While access may be restricted to specific employee groups, public sector funds provide strong security and tailored retirement solutions aligned with government employment.

Media

Mentions

Disclaimer: The information provided is of a general nature only and should not be construed as any form of advice. Readers are encouraged to seek appropriate independent financial advice before acting on any content herein.